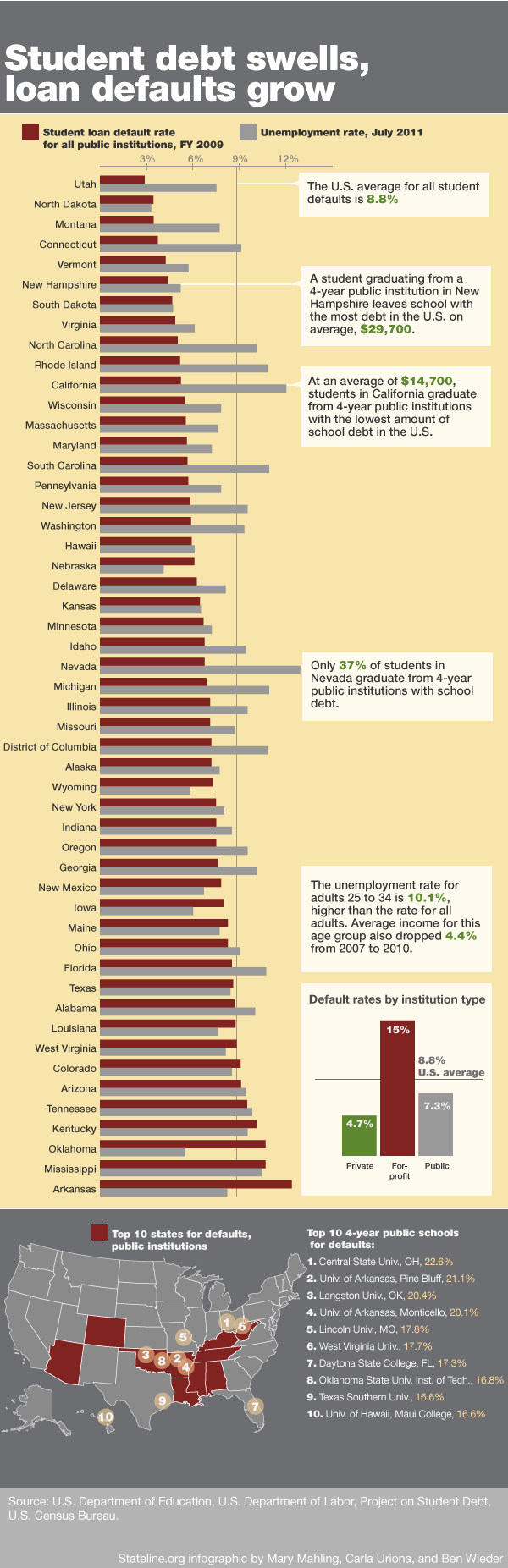

Student loans are a nuisance to most college students, especially in this economy and job market. So the statistics presented in the infographic below shouldn’t come as a surprise. According to the graphic, 8.8 percent of students find that their loans are in default and as the unemployment rate rises from state to state, so does the default rate of student loans.

You can also see from the infographic which states have the highest rate of student loans in default and which have the lowest. Students that attended a 4-year public university in New Hampshire left school with the highest debt in the U.S. with $29,700 in loans on average. At the same time, students graduating in California from the same type of public institutions leave with the lowest loans at $14,700 on average. Furthermore, although Nevada has one of the highest unemployment rates, only 37 percent of its students graduate with school loan debt.

Recent survey reports that state how employers plan to hire 9.5 percent more college graduates than last year comes at a time when students really need the help.

SOURCE & IMAGE: Visual.ly

Add comment